Mapping the digital finance landscape

The modern consumer ecosystem guide reveals a financial environment that no longer fits into neat, separate boxes. Traditional banking, insurance, and investment silos are dissolving. Instead, we are seeing a unified infrastructure where Web3 protocols, digital identity verification, and decentralized ledgers operate together. This integration changes how you manage risk and evaluate tools.

Think of this ecosystem like a city’s utility grid. In the past, electricity, water, and gas came from separate companies with distinct meters. Today, smart grids manage these flows simultaneously, responding to demand in real time. Similarly, your financial data now moves across platforms that verify identity and execute transactions in the same breath. The consumer’s guide to this digital ecosystem emphasizes navigation over ownership; you are moving through a network, not just holding assets in a vault.

Official frameworks, such as those from CGAP, stress an ecosystem approach to consumer protection. This means safeguards are built into the infrastructure itself, rather than relying solely on individual institutions. The EU Reporter’s recent analysis of the new online standard highlights how this shift requires a new literacy. You must understand how data flows between decentralized nodes and traditional banks to truly evaluate the tools you use.

Understanding this structural shift is the first step in the 2026 consumer ecosystem guide. It moves the conversation from simple product comparison to evaluating the integrity and connectivity of the underlying infrastructure. The following sections break down the specific tools that leverage this integrated model.

Core infrastructure layers

Understanding the consumer ecosystem guide requires looking past the shiny apps to the plumbing underneath. The technical stack consists of three distinct layers that work together to move value and data securely. Without this foundation, the consumer experience would be fragmented and risky.

Blockchains as the settlement layer

Blockchains act as the immutable ledger for the entire ecosystem. They provide the single source of truth for transactions, ensuring that records cannot be altered retroactively. This transparency is what allows different financial products to interoperate without needing a central intermediary to reconcile data.

Oracles for real-world data

Smart contracts are blind to outside events. Oracles bridge this gap by feeding real-world data—like exchange rates or weather conditions—into the blockchain. This connection allows decentralized applications to execute complex logic based on actual market conditions, making them useful for everyday consumers rather than just crypto traders.

Wallets as the user interface

The wallet is where the consumer meets the infrastructure. It manages private keys, signs transactions, and displays asset balances. Modern wallets are evolving from simple storage tools into full-fledged gateways that abstract away the underlying complexity of the blockchain layers below.

Essential tools for ecosystem navigation

Navigating the digital ecosystem requires more than just an internet connection; it demands the right infrastructure to manage identity, assets, and security. As the digital landscape shifts toward decentralized models, consumers and businesses need reliable tools that prioritize safety without sacrificing usability. The goal is to build a toolkit that protects your data while allowing seamless interaction across platforms.

Hardware wallets for asset security

For anyone holding digital assets, a hardware wallet is the first line of defense. These devices store private keys offline, keeping them isolated from online threats like phishing or malware. When choosing a wallet, look for open-source firmware and a strong track record of security audits. Brands like Ledger and Trezor dominate the market, but the specific model matters less than the habit of keeping funds cold.

As an Amazon Associate, we may earn from qualifying purchases.

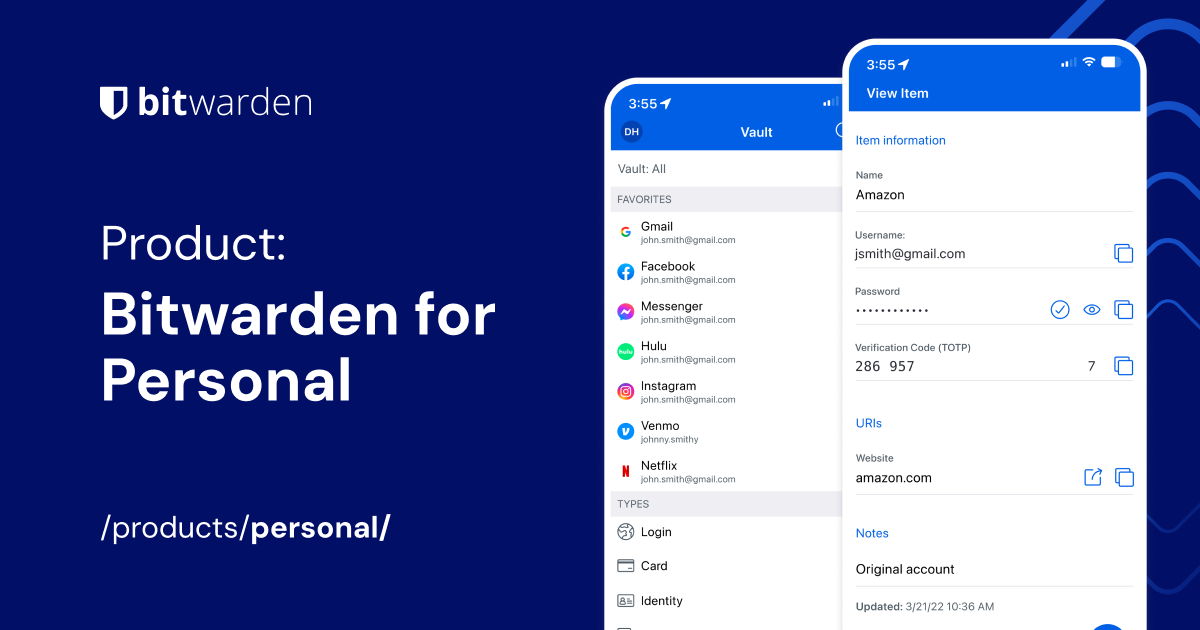

Secure password management

Identity is the new currency in the consumer ecosystem. A robust password manager is non-negotiable for maintaining separate, complex credentials for every service you use. Look for tools that offer zero-knowledge architecture, ensuring that even the provider cannot see your data. Integration with biometric authentication on mobile devices adds a layer of convenience without compromising security.

As an Amazon Associate, we may earn from qualifying purchases.

Network monitoring and privacy

Finally, securing your connection is critical. A Virtual Private Network (VPN) encrypts your traffic, preventing ISPs and third parties from tracking your activity. For businesses, enterprise-grade solutions offer additional features like split tunneling and dedicated IP addresses. Consumers should prioritize providers with a strict no-logs policy and servers in multiple jurisdictions to ensure data sovereignty.

Feature comparison

Choosing the right tools often comes down to specific needs. The table below highlights key differences between popular options to help you decide.

| Tool | Security Focus | Best For |

|---|---|---|

| Hardware Wallets | Offline key storage | Crypto assets |

| Password Managers | Zero-knowledge encryption | Digital identity |

| VPNs | Traffic encryption | Network privacy |

Build a resilient adoption strategy

Adopting new financial tools requires more than just downloading an app; it demands a structured approach to risk management and long-term utility. The goal is to integrate these technologies into your life without exposing yourself to unnecessary volatility or security gaps. Think of this process like building a foundation for a house: you need a solid base before you add the decorative elements.

Start by evaluating the infrastructure behind the tool. Is it backed by established institutions or experimental startups? Use official sources like CGAP to understand the consumer protection landscape. This ensures you are not just betting on a feature, but on a sustainable ecosystem that prioritizes your security over speculative gains.

By following this structured path, you shift from passive user to informed participant. This resilience protects your assets and ensures that your adoption of the consumer ecosystem is driven by utility and safety, not hype.

No comments yet. Be the first to share your thoughts!